Opening

This is something I come across regularly.

A taxpayer has been employed for years. Their employer deducts PAYE every month. As a result, tax has never been an issue.

Then, without any obvious change, there is suddenly an outstanding amount with SARS. SARS applies penalties. In some cases, SARS appoints the employer to deduct the debt directly from the salary.

At that point, the taxpayer has no idea what happened.

The visit to SARS

In most of these situations, the first step is a visit to a SARS branch.

The outcome is usually the same:

- SARS confirms the outstanding amount

- The taxpayer makes a payment

- This resolves the immediate problem

However, the underlying issue is not addressed.

The taxpayer leaves with the impression that it was a once-off problem — or possibly even a mistake.

What is not explained clearly is:

- Firstly, why it happened

- and secondly, that it is likely to happen again

Why you suddenly owe SARS money

In many of these cases, the taxpayer’s investment income has been growing steadily over time.

In the early years, the interest earned falls below the annual exemption. For the current tax year, this exemption is R23,800 for individuals under 65 and R34,500 for those 65 and older.

During that period, there is often no obligation to submit a return and no additional tax to pay.

But investments grow.

And at some point, the interest income crosses a level where the position changes.

The R30,000 threshold

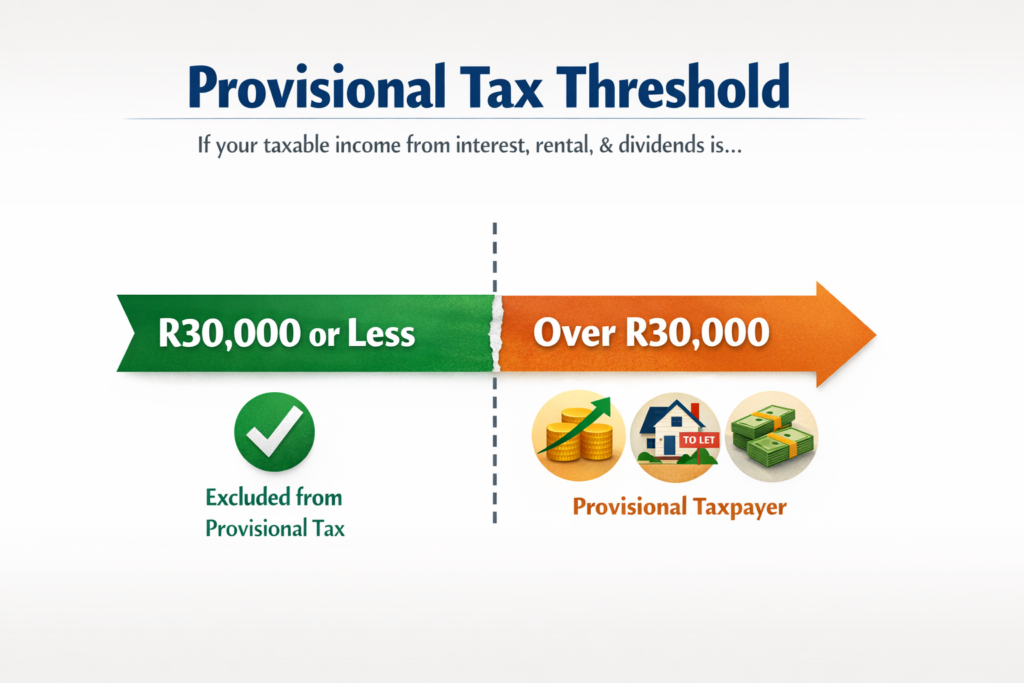

Under SARS rules, a salary earner who does not carry on a business is excluded from being a provisional taxpayer — but only if their taxable income from interest, foreign dividends, rental, and remuneration from an unregistered employer does not exceed R30,000 for the year. https://www.sars.gov.za/types-of-tax/provisional-tax/

Once the taxable interest alone exceeds that amount, the exclusion no longer applies.

In other words, the taxpayer is now, by definition, a provisional taxpayer.

What this means in practice

For example, consider a common scenario.

A taxpayer earns R350,000 in interest per year.

After the exemption of R23,800, the taxable interest is R326,200.

Obviously, this is well above the R30,000 threshold.

As a result, that taxpayer now needs to:

- submit provisional tax returns

- make at least two payments during the year — one by the end of August and one by the end of February

If these returns are not submitted, SARS can impose administrative penalties ranging from R250 to R16,000 per month, depending on taxable income. Furthermore, these penalties recur every month the return remains outstanding, for up to 35 months. https://www.sars.gov.za/types-of-tax/administrative-penalties/

Consequently, this is usually where the debt originates.

Not from a mistake.

Rather, from a change in status that was never recognised.

The reaction

“This must be incorrect. A tax practitioner will sort it out.”

In most cases, the assumption is that the outcome can be reversed.

However, it usually cannot.

The obligation was valid. SARS applied the penalties because the returns were not submitted. The tax fell due because the income exceeded the thresholds.

The next difficulty

Once the position is explained, the conversation usually moves to provisional tax.

And this is precisely where resistance sets in.

“I must now pay tax twice a year?”

“On money I do not have as cash?”

“It is interest — it is not money in my hand.”

This reaction is understandable.

After all, the interest is accruing, not being received as a monthly payment. In other words, the taxpayer does not experience it as income. But from a tax perspective, it is.

And provisional tax is not a separate tax. In essence, it is simply a mechanism to pay the normal income tax liability in advance, spread across the year, rather than accumulating a large debt at assessment.

The cycle that follows

This is often the part that is hardest to accept.

The taxpayer now has to:

- pay provisional tax on interest that is growing but not yet in hand

- simultaneously continue paying PAYE through their employer on their salary

And it does not end there.

Eventually, when the investments mature or the taxpayer retires:

- monthly pension or annuity income will be taxable, with PAYE deducted by the fund

- in addition, any lump sum taken at retirement is taxed according to SARS tables, with the first R550,000 tax-free and the balance taxed at rates up to 36%

- and if the remaining investments continue to earn significant interest, provisional tax obligations may continue into retirement

As a result, it feels like an endless cycle of paying.

And in many ways, it is.

The temptation to react

One response I have seen is the desire to withdraw money or restructure investments purely to avoid the tax.

“I would rather take the money out and keep it where SARS cannot see it.”

However, this is a reaction to the frustration — not a solution to the underlying position.

The tax arises because the income exists. Therefore, moving money does not change the obligation retrospectively, and it does not address the structural issue going forward.

What needs to happen

The focus should not be on making the tax go away.

Instead, it should be on:

- understanding that the obligation exists

- accepting that the taxpayer’s status has changed

- and putting a structure in place to manage the payments in a controlled way

For investment planning — specifically how to structure savings more efficiently, which products to use, how to balance growth with tax exposure — that is the role of a financial adviser.

From a tax perspective, however, the focus is narrower:

- firstly, why this happened

- secondly, what the current obligations are

- and finally, how to manage them going forward so the situation does not repeat itself

Closing

This is not an unusual situation.

In fact, it arises whenever investments have grown over time and the tax position has not been reassessed alongside that growth.

The difficulty is not the amount owed.

Rather, it is the shift in understanding:

from “my tax is handled” to “I owe SARS money because my situation changed and now requires active management.”

That shift is often uncomfortable. But it is necessary.

Because the system does not adjust itself. Instead, the taxpayer’s approach to compliance has to adjust.